Press Release

Hong Kong, 12th March 2026

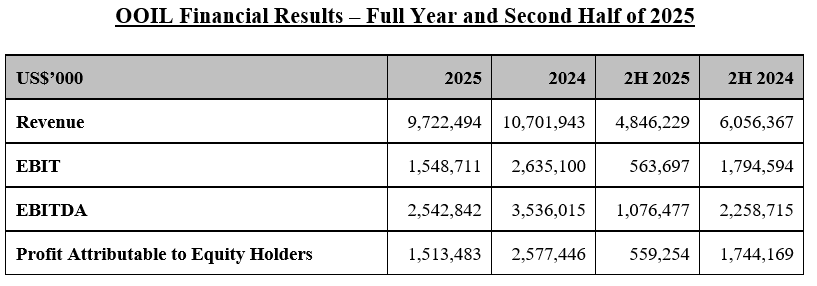

Orient Overseas (International) Limited Announces 2025 Full Year Results

-

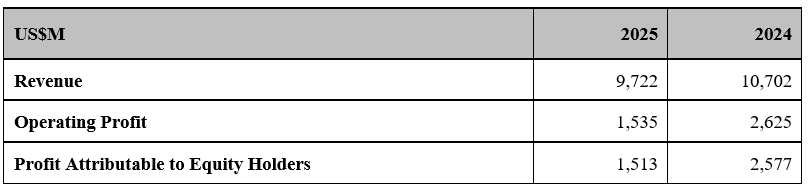

Group Revenue of US$9,722 million

-

Group EBIT of US$1,549 million

-

Group EBITDA of US$2,543 million

-

Operating Cash Flow of US$1,991 million

-

Profit Attributable to Equity Holders of US$1,513 million

-

Recommended Dividend for Full Year 2025 is approximately 50% of the Profit Attributable to Equity Holders at approximately US$753 million, with proposed Final Dividend of US$0.42 per ordinary share

Financial and Operational Highlights – Full Year 2025

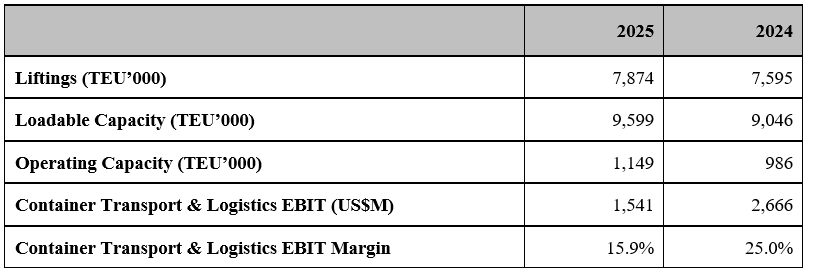

- Container Transport and Logistics business reported EBIT of US$1,541 million, representing an EBIT margin of approximately 15.9%

- Liner liftings grew to 7.9 million TEU

- Ordered fourteen 18,500 TEU class methanol dual fuel container vessels which are expected to be delivered between 2028 and 2029

Balance Sheet Highlights

- Group financial position remains one of the most robust in the industry

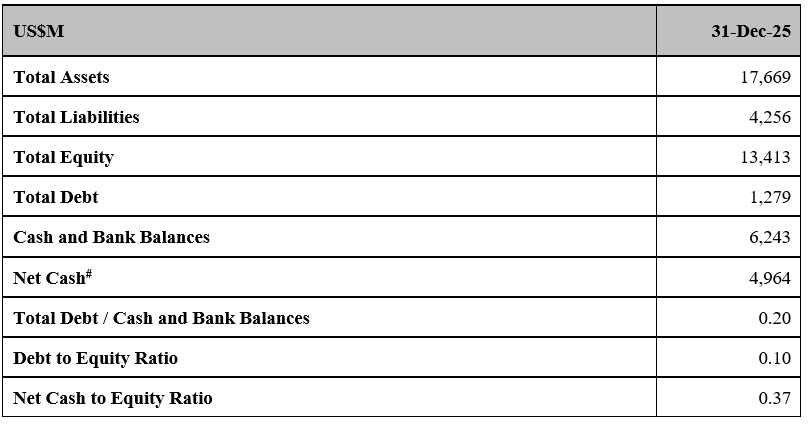

- Net cash of US$5.0 billion as at 31st December 2025

- Cash and bank balances of US$6.2 billion as at 31st December 2025

# Net cash represents cash and bank balances deducted by total debt.

Details

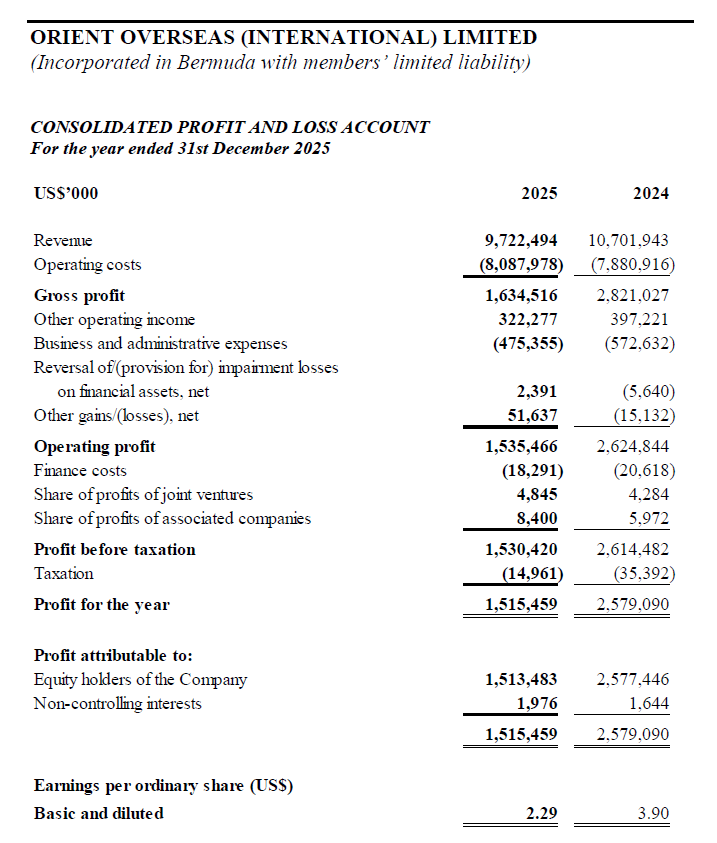

Orient Overseas (International) Limited (“OOIL") today announced a profit attributable to equity holders of US$1,513.5 million for 2025, compared to a profit of US$2,577.4 million in 2024.

Earnings per ordinary share in 2025 was US$2.29, whereas earnings per ordinary share in 2024 was US$3.90.

The Board of Directors has recommended that the dividend for full year 2025 is approximately 50% of the profit attributable to equity holders at approximately US$753 million, with proposed payment of a final dividend of US$0.42 per ordinary share for 2025. The final dividend will be payable in cash in US dollars or Hong Kong dollars (HK$3.276 converted at the exchange rate of US$1 to HK$7.8) or Renminbi (to be converted at the average of middle exchange rate between US dollars and Renminbi as announced by the People's Bank of China for the 5 business days before and excluding the date of the annual general meeting of the Company).

In 2025, the global economy moved unpredictably amid shifting and uncertain policy environments. Tariff measures and trade tensions continued to weigh heavily on the container shipping industry, most notably on the Trans‑Pacific trade, driving sharp fluctuations in both cargo volumes and freight rates. At the same time, policy adjustments and front‑loading disrupted the usual post Lunar New Year seasonal patterns. Heightened expectations of strong profit margins intensified competition on certain routes, amplifying market volatility and creating significant operational challenges for carriers, shippers, and freight forwarders. Entering November, tariffs and port charges imposed under the USTR 301 investigation were suspended. Although uncertainty persisted over whether tariffs would be reinstated, the one-year suspension offered temporary relief to market sentiment. As the traditional year‑end peak season approached, the container shipping market began to recover gradually.

Although global economic growth slowed in 2025, several emerging markets, such as Africa, South Asia, and Southeast Asia, continued to show strong growth momentum. This may have been driven by shifts in trade patterns that boosted local trade, or by domestic economic expansion stimulating local demand. It is also possible that spillover effects from other markets simply require more time to materialise. Regardless of the reason, we have seen carriers seize this opportunity to accelerate the deployment and adjustment of their service networks.

In a rapidly changing market environment, we remain firmly committed to implementing proactive, flexible, and forward‑looking management strategies to address uncertainties. While strengthening our East-West service networks, we are also adapting to shifts in global trade patterns, seizing new growth opportunities, accelerating investment in emerging markets, and striving to achieve a more balanced global presence to mitigate risks arising from individual regional markets.

In 2025, we took delivery of nine brand‑new 16,828 TEU container vessels, completing the full delivery of the entire 16,828 TEU series, all of which have now entered service. This has not only strengthened our capabilities on the Trans‑Pacific trade, but the additional capacity also indirectly enabled the resumption of the LL3 service on the Asia-Europe trade, which had previously been suspended due to capacity shortages, further meeting our customers' expectations for consistent, high‑quality service. In 2026, more new vessels will join our fleet, including the long‑awaited 24,000 TEU class methanol dual fuel container vessels and 13,580 TEU class conventional fuel vessels chartered from subsidiaries of Seaspan Corporation. The addition of these vessels will support the continued expansion and upgrading of our fleet, enabling us to build a more efficient, environmentally friendly, intelligent, and wider‑coverage service network for our customers. Moreover, the delivery of the dual fuel vessels marks an important milestone in OOCL's decarbonisation journey.

Our cooperation with COSCO SHIPPING Lines continues to deepen. In recent years, the synergy of the dual‑brand strategy has enabled OOCL to make significant progress in cost optimisation and risk diversification, laying a solid foundation for the Group's stable operations. These synergies will continue to play their role in the new year.

We are accelerating our vertical expansion of the supply chain by offering customised solutions such as international order processing, cargo management, warehousing, and distribution services. These efforts enable us to build an end‑to‑end intelligent and digitalised supply chain that delivers high‑value services for our customers, further fulfilling our Customer Focus commitment.

Digitalisation has become integral to our services and operations, serving as a powerful tool to strengthen cost control, enhance management efficiency and user experience, and maintain our competitiveness. Through our collaboration with GSBN, we are also working with other stakeholders to advance the development of a fully digitalised supply chain and foster a smart and healthy global trade ecosystem.

Looking ahead, the International Monetary Fund forecasts global economic growth will remain unchanged at 3.3% in 2026 compared to 2025, and reach 3.2% in 2027. Under this slower‑growth outlook, structural overcapacity and the resumption of Red Sea transits are expected to exert considerable pressure on freight rates. Regional economic imbalances, fluctuations in tariff policies, and ongoing geopolitical tensions will continue to disrupt supply chain stability and reshape global trade patterns. Meanwhile, the postponement of the IMO's net‑zero framework vote and the expansion of the EU Emissions Trading System, requiring shipping companies to report 100% of their emissions from 1st January 2026, may increase operation complexity and costs of shipping companies. All these factors will bring immediate as well as broad and long‑term implications to the container shipping sector.

As we entered 2026, some carriers have at one point routed certain services or vessels through the Red Sea, and new vessel deliveries continue to increase. Concerns over excess capacity have resurfaced, yet the charter market remains exceptionally tight with vessels in extremely short supply, and changes in the Middle East situation have added further uncertainty to future market developments. Effective capacity management therefore remains a central focus for the industry. Meanwhile, geopolitical developments are occurring with increasing frequency, and where any single event may take effect instantly and create far‑reaching ripple impacts, it has become increasingly difficult to forecast market trends with precision. The only prudent course is to stay focused on our own fundamentals, act with caution, adapt to evolving conditions, and respond proactively.

OOCL will continue working closely with COSCO SHIPPING Lines to maintain our top echelon's position in the industry. Leveraging the advantages of the dual‑brand strategy, we will continue optimising cost control; uphold our customer focus philosophy; proactively explore markets; further enhance service network flexibility, service reliability, and operational stability; strengthen resilience against risks; and work together with all stakeholders to build a high‑quality, end‑to‑end green supply chain network.

As at 31st December 2025, the Group had cash and bank balances of US$6,243.2 million compared with debt obligations of US$568.4 million repayable in 2026. The Group had a net cash to equity ratio of 0.37 : 1 as at end of 2025, compared with 0.49 : 1 at the end of 2024. The Group from time to time prepares and updates cashflow forecasts for asset acquisitions, to serve project development requirements, as well as working capital needs, from time to time with the objective of maintaining a proper balance between a conservative liquidity level and an effective investment of surplus funds.

OOIL owns one of the world's largest international integrated container transport businesses which trades under the name “OOCL". With over 430 offices in more than 90 countries/regions, the Group is one of Hong Kong's most international businesses. OOIL is listed on The Stock Exchange of Hong Kong Limited.

* * *

Issued by: Orient Overseas (International) Limited

For further information contact

Martin Kan Investor Relations (852) 2833 3143

Website: https://www.ooilgroup.com